Source: Estimates for third relief bill based on bill text, committee and administration numbers.

Credit: Audrey Carlsen/NPR

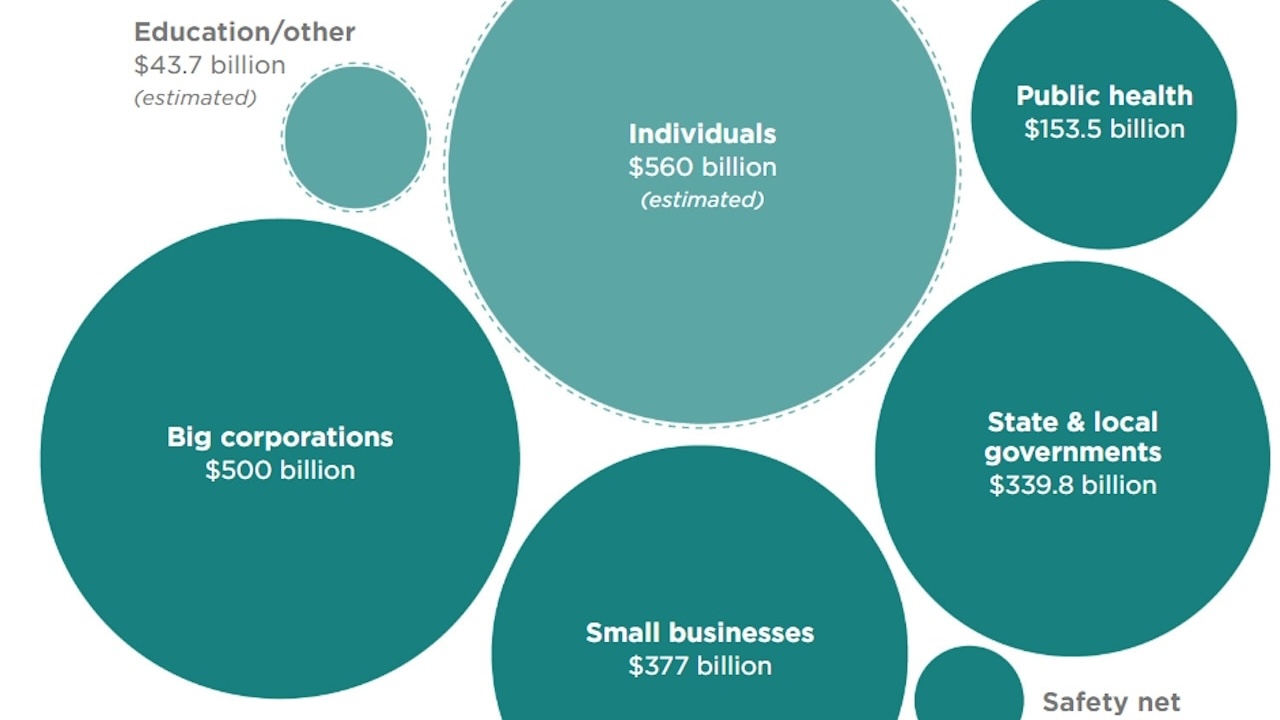

The Senate developed $2 Trillion dollar, multi-faceted legislation attacking this disaster from multiple sides: tax and debt relief, small business loans, unemployment expansion, and individual stimulus payments. They see we’re hurting and they aren’t playing around.

Incentive and assistance for small businesses to keep employees working

The bill creates a “paycheck protection program” for:

- Self-employed individuals

- Small businesses

- “Gig economy” workers

Hey solopreneurs and giggers, you finally aren’t being excluded from the group and chastised for being your own boss! Congratulations!

Let’s take a big bite and jump in.

INDIVIDUAL TAXES

They will need your individual 2019 taxes (and valid social security numbers) in order to cut you a check for $1200 and $500 for each child under 17. No tax liability limits or minimum income qualifier. (Just be sure that your ex isn’t trying to claim them too, that is still first come first serve.)

Is your AGI (Adjust Gross Income) over $99,000 single or $150,000 married filing jointly? Check out this break down by Forbes article on the CARES Act

No double-dipping

Now, you will need to assess your tax liability for 2021. Because the Senate lit a fire and got this bill enacted now instead of making everyone cash in next year during tax time, and send the economy into a tailspin, these checks are considered ADVANCED PAYMENT on a credit that will be available for 2021. This is where your handy CPA comes into play to advise you based on your current situation. Most of the nation is in agreement – need cash now.

SMALL BUSINESS LOANS

Small business under 500 (the ones that got the bad news with the FFCRA about paying their employees for sick leave and extended family and medical leave for up to 12 weeks?) it’s your time to breathe a little, they have your back. You will now have access to $350 billion in 100% federally guaranteed “paycheck protection loans.” I know, I hear you groaning. Loans mean principal and interest and get the shovel and the ladder for this giant hole I’m about to dig. Hang in there! They built in some debt relief for you too.

This provision would provide an 8 week period from the start of the loan for cash flow assistance to maintain payroll, interest on mortgage, rent, and utilities on a tax-free basis. “For six months, SBA is required to pay all principal, interest and fees on all existing SBA loan products including 7(a), Community Advantage, 504, and Microloan programs for six months.” There will be a lot of documentation to be submitted for all this, don’t forget who you are dealing with. Stay organized so you get maximum savings!

The proposal will be enacted retroactively back to February 15th when things really started to hit the fan and you had to make the tough decision to let some of your people go. Time to get on the phone and get them back! The maximum maturity of the loan is 10 years, no more than 4% but currently the rate is at 3.75% depending on your situation.

Covered payroll costs are:

- What you pay your employee or independent contractor (hourly, tips, commission etc)

- Regular paid leave (vacation, sick, medical, parental)

- Health care or retirement benefits

- State/local taxes when you pay your employee or independent contractor

What they are not:

- Payroll taxes

- compensation over $100,000 (up to but not over)

- Sick/medical leave you are already getting a credit for thanks to the FFCRA signed last week (no double dipping, remember?)

- Compensation for employees outside the U.S.

- The Venti latte from Starbucks you need while you approve payroll so you don’t face plant on the desk while calling that one employee that never has their time submitted

Economic Injury Disaster Loans/Grants

Small businesses under 500 employees, sole proprietors and ESOP’s will have access to emergency disaster loans and grants for help outside of payroll costs with no personal guarantee required under $200k. If you apply for a loan, you can get a grant for an immediate advance up to $10k to maintain payroll and does not need to be repaid.

UNEMPLOYMENT EXPANSION

- Additional $600/week on top of base payments for 4 months

- 13 week extension to maximum

- Temporary Pandemic Unemployment Assistance program through 2020 for self-employed, gig workers, freelancers and contractors

- 7-day waiting period is waived, immediate filing available

TAX PROVISIONS

(Insider tip: call a CPA to interpret the details so your brain doesn’t go to mush)

Using Retirement funds

There are many events in life that make the possibility of taking funds from retirement accounts to dig ourselves out extremely alluring. Until you see the 10% price tag that comes with it.

There is now a special rule called a “coronavirus-related distribution” that allows you to take a distribution up to $100k for 2020 only, PENALTY FREE. The qualifiers are if you, a spouse, or dependent is diagnosed with SRS-COV-2 or Covid-19 by a CDC-approved test or experience financial consequences due to:

- Being quarantined

- Furloughed, laid off, or reduced work hours

- Inability to work due to lack of child care

HOWEVER, you will still be required to pay income tax (over a 3 year period) and run the risk of putting yourself in a pickle come retirement time if you don’t replace it and miss out on the interest. Talk to your financial advisor and choose wisely based on your current situation.

Qualified Improvement Property

The provision enables businesses, especially in the hospitality industry, to write off immediately costs associated with improving facilities instead of having to depreciate those improvements over the 39-year life of the building. The provision, not only increases companies’ access to cash flow by allowing them to amend a prior year return, but also incentivizes them to continue to invest in improvements as the country recovers from the COVID-19 emergency. (CARES Act, U.S. Senator Cory Gardner)

Charitable Contributions

- Standard deduction increased (Originally $12,400 single, $24,800 for married filing jointly)

- Ability to make a cash contribution of $300 in addition to the standard deduction if you do not itemize your deductions

- Only applies to qualified charities

- For the individuals that itemize their deductions, the CARES Act will allow contributions up to 100% of your Adjusted Gross Income (instead of the standard 60%) for 2020 and excess contributions to be carried over to the next 5 years

- Increase from 10% to 25% for corporate donors

Employee Student Loan Debt

- Employers can pay up to $5250 to an employees student loan debt on a tax-free basis without employee having to claim as taxable income

- However, employee cannot deduct student loan interest come tax time

Employee Retention Credit

This may be my favorite part of the bill.

Ladies and Gentlemen! For one year only! I give you… the Employee Retention Credit.

If your business is forced to suspend or close your operations due to Covid-19 and you continue to pay your employees during the shut down, you can qualify for a 50% employee retention credit as an incentive to keep employees on your payroll.

You can qualify for a credit against your 6.2% share of the Social Security payroll tax if:

- The operation of the business was fully or partially suspended during any calendar quarter during 2020 due to orders from an appropriate government authority resulting from COVID-19, or

- The business remained open, but during any quarter in 2020, gross receipts for that quarter were less than 50% of what they were for the same quarter in 2019. The business will then be entitled to a credit for each quarter, until the business has a quarter where it’s recovered sufficiently that its receipts exceed 80% of what they were for the same quarter in the previous year

The credit is provided for the first $10,000 of compensation, including health benefits, paid to an eligible employee. The credit is provided for wages paid or incurred from March 13, 2020 through December 31, 2020.

There is also a provision providing access to paid leave by employees that were laid off March 1st or later, if they are rehired. However, they would need to have worked for the employer at least 30 days prior to being laid off.

Delayed payment of employer payroll and self-employment tax

- Defer payment of the employers share of the Social Security tax they would otherwise be responsible to pay

- Deferred payment can be paid over the following 2 years (half paid by 12-31-2021, the other half paid by 12-31-2022)

Net Operating Loss Modifications

Net operating losses (NOL) are currently subject to taxable-income limitations and cannot be carried back to reduce income in a prior tax year.

This provision would allow

- A NOL beginning in 2018, 2019, or 2020 to be carried back 5 years

- Temporarily removes taxable income limit to fully offset income 100% (up from 80%)

- Ability to utilize loss and amend prior year returns to provide critical cash flow and liquidity during Covid-19 emergency

Interest Limitation Rules

Increased interest limitation from 30% to 50% of adjustable taxable income for 2019 and 2020

We went live on facebook with HR Branches and Gilbertson Law Office to break this down for you. Watch it here:n

Follow our Facebook page to get updated when we go live and stay in the know:

Or sign up for our email newsletter at the bottom of the page.